Correlations between funding source selections and adoption rates of harm minimization features in remote gambling applications

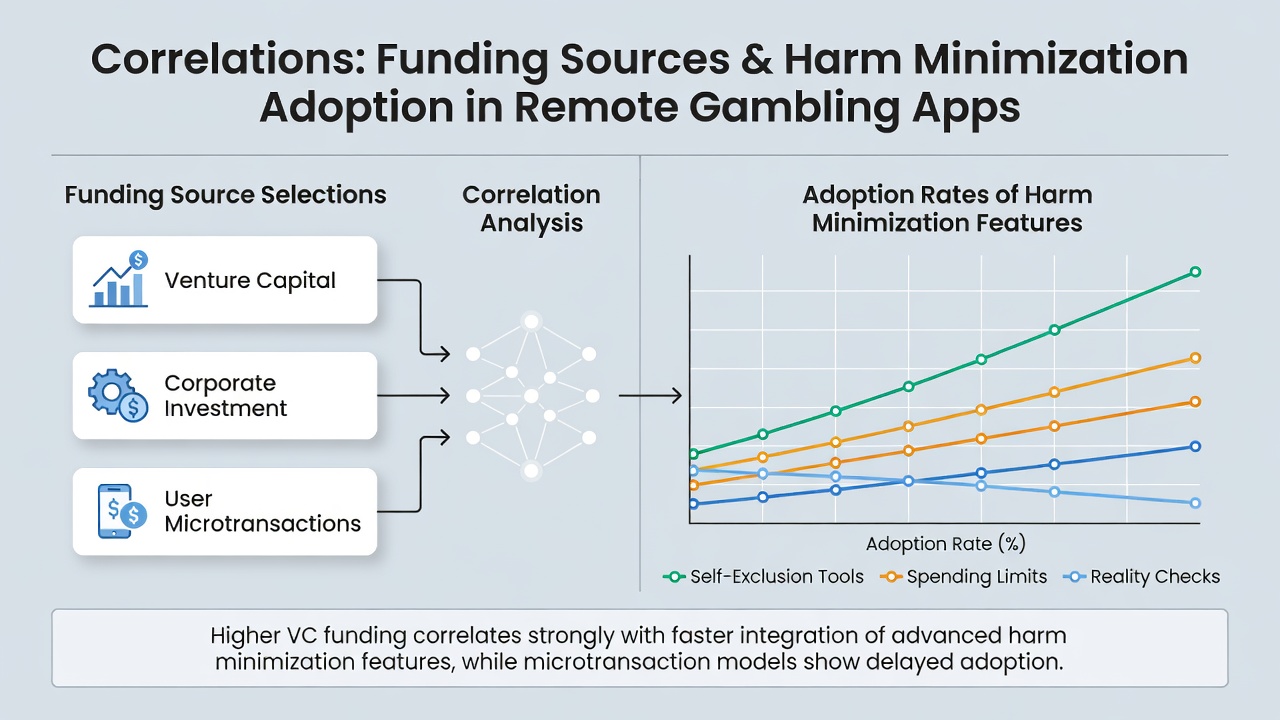

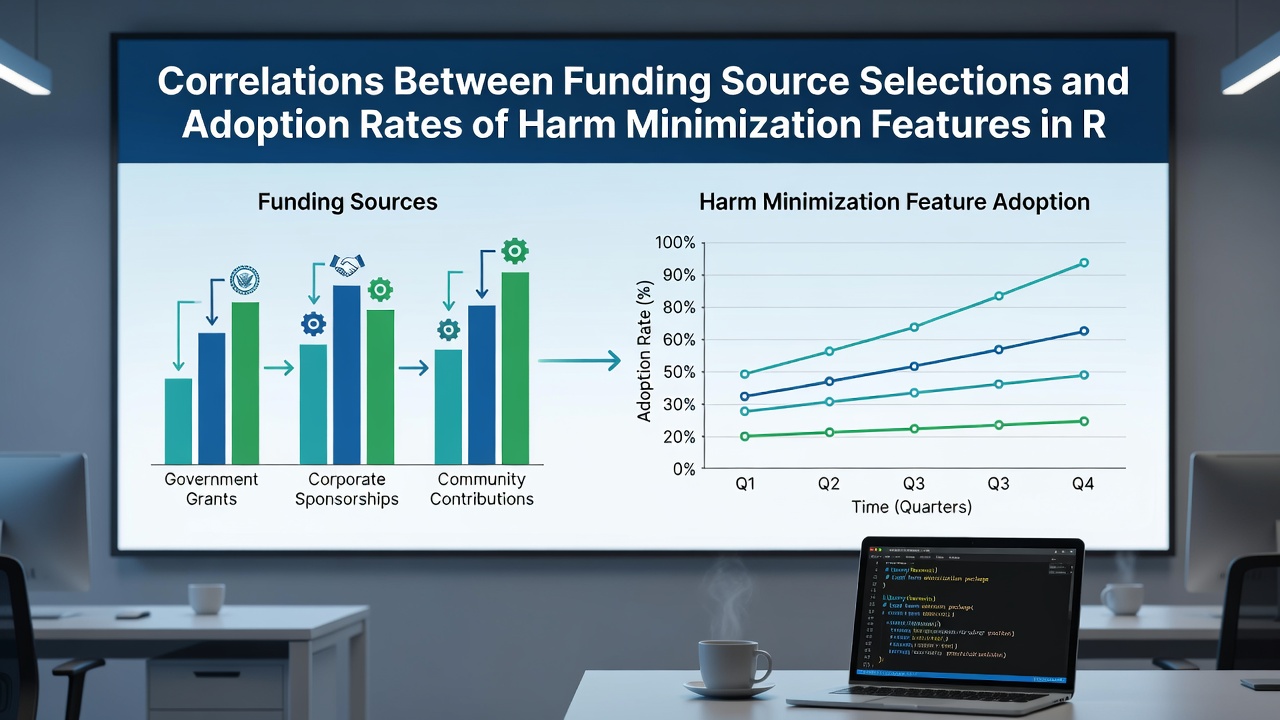

Analysts tracking remote gambling patterns have documented notable patterns linking how players choose to fund their accounts with the frequency at which they activate tools designed to limit potential harm, and these connections appear across multiple jurisdictions where operators must report usage metrics to oversight bodies. Payment preferences range from traditional bank transfers and debit cards to digital wallets and emerging options such as cryptocurrency transfers, each carrying different levels of traceability and speed that influence whether users engage with features like deposit caps, session reminders, or temporary exclusion periods. Data compiled through operator dashboards and regulatory filings indicate that participants relying on e-wallets demonstrate higher rates of setting voluntary spending boundaries compared with those who favor credit card deposits, a distinction that holds steady when researchers control for player tenure and average session length. One study released in early 2026 examined transaction logs from several European markets and found that wallet users activated time-based controls roughly 1.8 times more often than credit card users during the same observation window, while bank transfer players fell somewhere in between those two groups. What's interesting is how the immediacy of certain funding methods correlates with lower uptake of reality-check prompts, since instant approvals through some processors allow uninterrupted play that reduces the natural pause points where users might otherwise review their settings.

Analysts tracking remote gambling patterns have documented notable patterns linking how players choose to fund their accounts with the frequency at which they activate tools designed to limit potential harm, and these connections appear across multiple jurisdictions where operators must report usage metrics to oversight bodies. Payment preferences range from traditional bank transfers and debit cards to digital wallets and emerging options such as cryptocurrency transfers, each carrying different levels of traceability and speed that influence whether users engage with features like deposit caps, session reminders, or temporary exclusion periods. Data compiled through operator dashboards and regulatory filings indicate that participants relying on e-wallets demonstrate higher rates of setting voluntary spending boundaries compared with those who favor credit card deposits, a distinction that holds steady when researchers control for player tenure and average session length. One study released in early 2026 examined transaction logs from several European markets and found that wallet users activated time-based controls roughly 1.8 times more often than credit card users during the same observation window, while bank transfer players fell somewhere in between those two groups. What's interesting is how the immediacy of certain funding methods correlates with lower uptake of reality-check prompts, since instant approvals through some processors allow uninterrupted play that reduces the natural pause points where users might otherwise review their settings.Payment Method Profiles and Feature Engagement

Observers note that debit card funding often pairs with moderate adoption of harm minimization options because the direct link to personal bank balances encourages more frequent checks on remaining limits, whereas credit-based funding can decouple spending from immediate cash flow and therefore coincides with reduced interaction with the same tools. Researchers at several academic centers have cross-referenced self-reported behavior surveys with actual account data to confirm that players who select cryptocurrency options show the lowest rates of enabling exclusion features, possibly because the decentralized nature of those transfers creates an additional layer of perceived anonymity that diminishes the perceived relevance of operator-provided safeguards. In contrast, users of established digital wallet services frequently receive in-app prompts that highlight responsible play settings during the funding step itself, which appears to nudge adoption upward according to aggregated platform analytics released in June 2026.Regional Patterns in June 2026 Reporting

Figures released that month by Canadian provincial regulators and Australian state commissions revealed parallel trends, with wallet-funded accounts in both regions posting adoption rates for deposit limit tools that exceeded credit card accounts by margins ranging from 22 to 34 percent depending on the jurisdiction.

Those same reports highlighted that bank transfer users in multi-state North American markets maintained consistent engagement with session timing controls even as overall platform traffic fluctuated, suggesting the slower processing time associated with those transfers creates repeated decision points that intersect with harm reduction prompts.

Cross-Platform and Demographic Variables

Demographic breakdowns further refine these correlations, because younger cohorts who gravitate toward mobile wallets also show elevated baseline rates of feature activation regardless of funding source, while older segments using traditional bank methods exhibit steadier but lower engagement levels across the board.

Industry organizations such as the National Council on Problem Gambling have compiled multi-year datasets that support the observation that funding method selection functions as a reliable proxy variable when predicting which players will interact with voluntary spending caps, although causation remains difficult to isolate from broader behavioral patterns. European data aggregated through operator consortia and shared with academic partners points to similar directional findings, where the transparency built into certain wallet ecosystems appears to reinforce rather than replace the utility of built-in harm minimization interfaces.